🔍 What Does Section 329 Say (in Simple Terms)?

Section 329 says that:

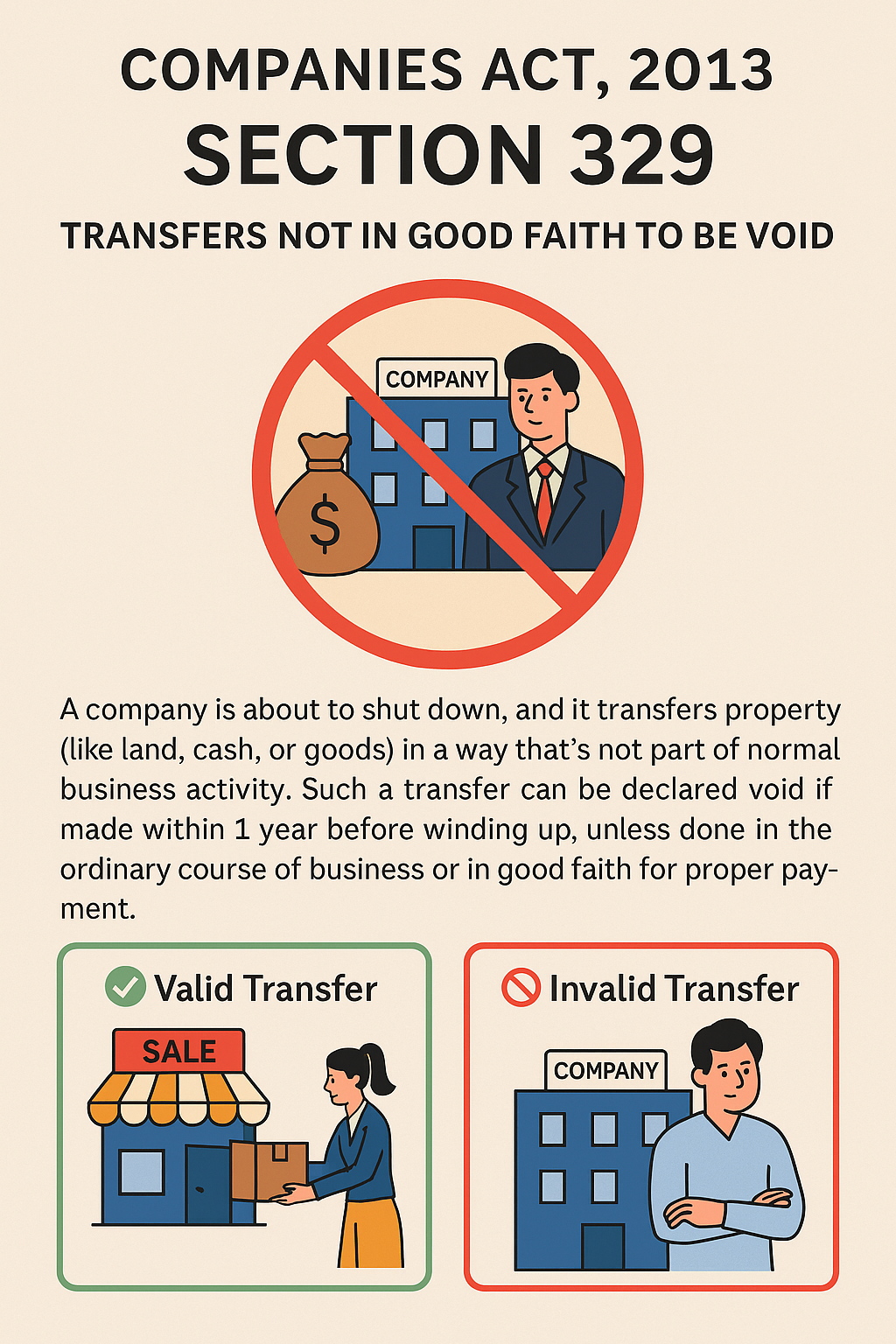

If a company is about to be closed down (wound up), and it transfers property (like land, buildings, cash, or goods) to someone in a way that isn’t normal business activity, then such a transfer can be declared invalid or void if done within 1 year before the start of the winding-up process.

But there are two exceptions:

The transfer was done in the ordinary course of business, OR

The transfer was made to a person who:

Acted in good faith, and

Paid fair value (proper price) for the property.

🧾 What Changed After the Amendment (2016)?

Before:

Section 329 applied only to winding up by Tribunal petition (i.e., compulsory winding up).

After Amendment (via IBC 2016):

It now also includes cases where a company voluntarily decides to wind up (voluntary winding up).

🧠 Why This Rule Exists?

To stop companies from:

Hiding assets

Favoring certain people (e.g., relatives or friends)

Avoiding paying off creditors just before shutting down!

📘 Examples to Understand Better

✅ Example 1: Valid Transfer

ABC Ltd. sells office furniture to a customer 6 months before filing for winding up.

It was a regular business sale.

The customer paid a fair price.

👉 This transfer is valid.

❌ Example 2: Invalid Transfer

XYZ Pvt. Ltd. transfers a company car to the director’s brother for free, 3 months before winding up.

Not in the course of business

No money paid (no valuable consideration)

Possibly done to keep assets out of liquidation

👉 This transfer is void (invalid) against the Company Liquidator.

❌ Example 3: Suspicious Timing

123 Industries sells its land to a third party 2 weeks before filing for winding up.

Even if money was paid, if it’s found that the buyer knew the company was going to shut down (i.e., not in good faith),

👉 This can also be declared void.

✅ In Short:

Any shady or suspicious transfer of assets done within 1 year before winding up can be cancelled by the liquidator.

Transfers are safe if they are:

Part of normal business, OR

Done honestly and with proper payment

Legal Text of Section 329 of Companies Act 2013

Transfers Not in Good Faith to be Void

[Any transfer of property, movable or immovable, or any delivery of goods, made by a company, not being a transfer or delivery made in the ordinary course of its business or in favour of a purchaser or encumbrancer in good faith and for valuable consideration, if made within a period of one year before the presentation of a petition for winding up by the Tribunal under this Act shall be void against the Company Liquidator.”]

Amendment

- (a) Substituted by Insolvency and Bankruptcy Code, 2016 Dated 15th November, 2016.

For section 329,

- Any transfer of property, movable or immovable, or any delivery of goods, made by a company, not being a transfer or delivery made in the ordinary course of its business or in favour of a purchaser or encumbrance in good faith and for valuable consideration, if made within a period of one year before the presentation of a petition for winding up by the Tribunal or the passing of a resolution for voluntary winding up of the company, shall be void against the Company Liquidator.

the following section shall be substituted, namely:—

“329. Any transfer of property, movable or immovable, or any delivery of goods, made by a company, not being a transfer or delivery made in the ordinary course of its business or in favour of a purchaser or encumbrancer in good faith and for valuable consideration, if made within a period of one year before the presentation of a petition for winding up by the Tribunal under this Act shall be void against the Company Liquidator.”.

(b) The MCA Notification No. F.O. 3453(E) Dated 15th November, 2016, enforcing the related sections of Insolvency and Bankruptcy Code, 2016.