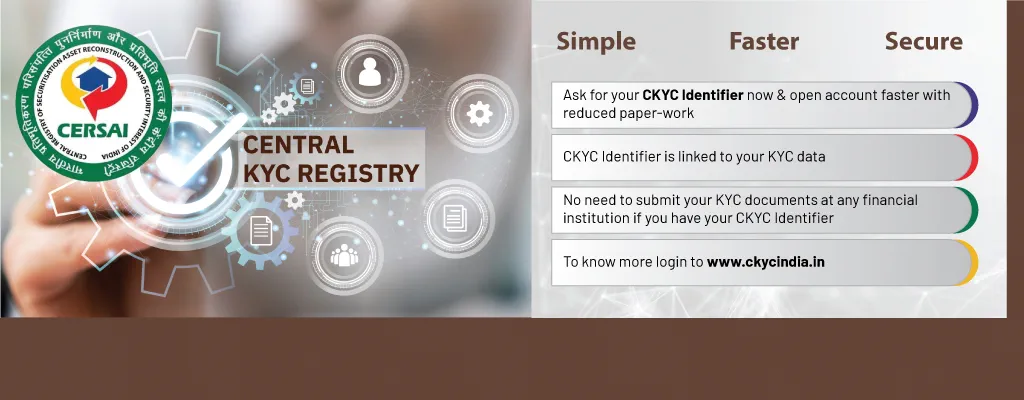

CKYC India

Central Know Your Customer (CKYC) is a centralized KYC repository introduced by the Government of India to simplify the KYC process across financial institutions. It eliminates the need to submit KYC documents multiple times for different financial services. Background of CKYC Section 73 of the Prevention of Money Laundering Act, 2002, gives the central government […]