(1) In computing income-tax on the total income of an assessee with which he is chargeable for any tax year, there shall be allowed from income-tax (as computed before allowing the deductions under this Part), subject to the provisions of section 156, the deductions specified therein.

(2) The deduction under section 156, shall not, in any case, exceed income-tax (as computed before allowing the deductions under this Part) on the total income of the assessee with which he is chargeable for any tax year

Section 155 – Overview & Interpretation

Text of Section 155:

Sub-section (1)

When computing income-tax on an assessee’s total income for any tax year, a deduction (i.e., rebate) shall be allowed from the computed income-tax (that is, after total income is assessed, but before deductions under this Part), subject to section 156.Sub-section (2)

The deduction under section 156 cannot exceed the income-tax amount computed before deducting under this Part.

This effectively means:

You first determine tax based on total income (before applying rebates/deductions under this Part),

Then you reduce the tax liability by allowed rebates (under section 156), but the rebate cannot exceed the tax due.

This mirrors principles seen previously—ensuring rebates don’t result in negative tax or exceed liability.

Analysis & Implications

1. Anti-abuse safeguard

Ensures fairness: Rebates cannot exceed tax liability, preventing unreasonable reductions.

Prevents refunds: If rebate > tax, one’s tax liability drops to zero, but no negative or refund benefit arises—keeping revenue neutral.

2. Coordination with section 156

Section 155 sets the broad framework; section 156 specifics eligible rebates (like charitable contributions, insurance premium rebates, etc.).

Together, they control the allowances that reduce the tax burden, while capping how far relief can go.

3. Simplicity and clarity

Offers clarity: step-based approach—compute tax → then rebate within limits.

Avoids complex cross-calculation between rebates and income.

4. Comparison with old law

Historically (under the 1961 Act), similar “rebate” structures like section 87A operated with caps.

This provision seems to generalize that approach for broader rebate categories in the new Act.

Example Illustration

Suppose your total income yields ₹100,000 tax (before rebates), and you’re entitled to a ₹120,000 rebate under section 156:

You can only deduct up to ₹100,000—bringing tax to zero.

The excess ₹20,000 rebate is effectively wasted, not refunded.

This ensures that rebates are tax-reducing, not tax-refunding.

In summary, Section 155 formalizes the sequence of tax computation—determine liability, then subtract rebates (within limit)—while safeguarding that rebates cannot generate a refund. It upholds fairness and administrative simplicity.

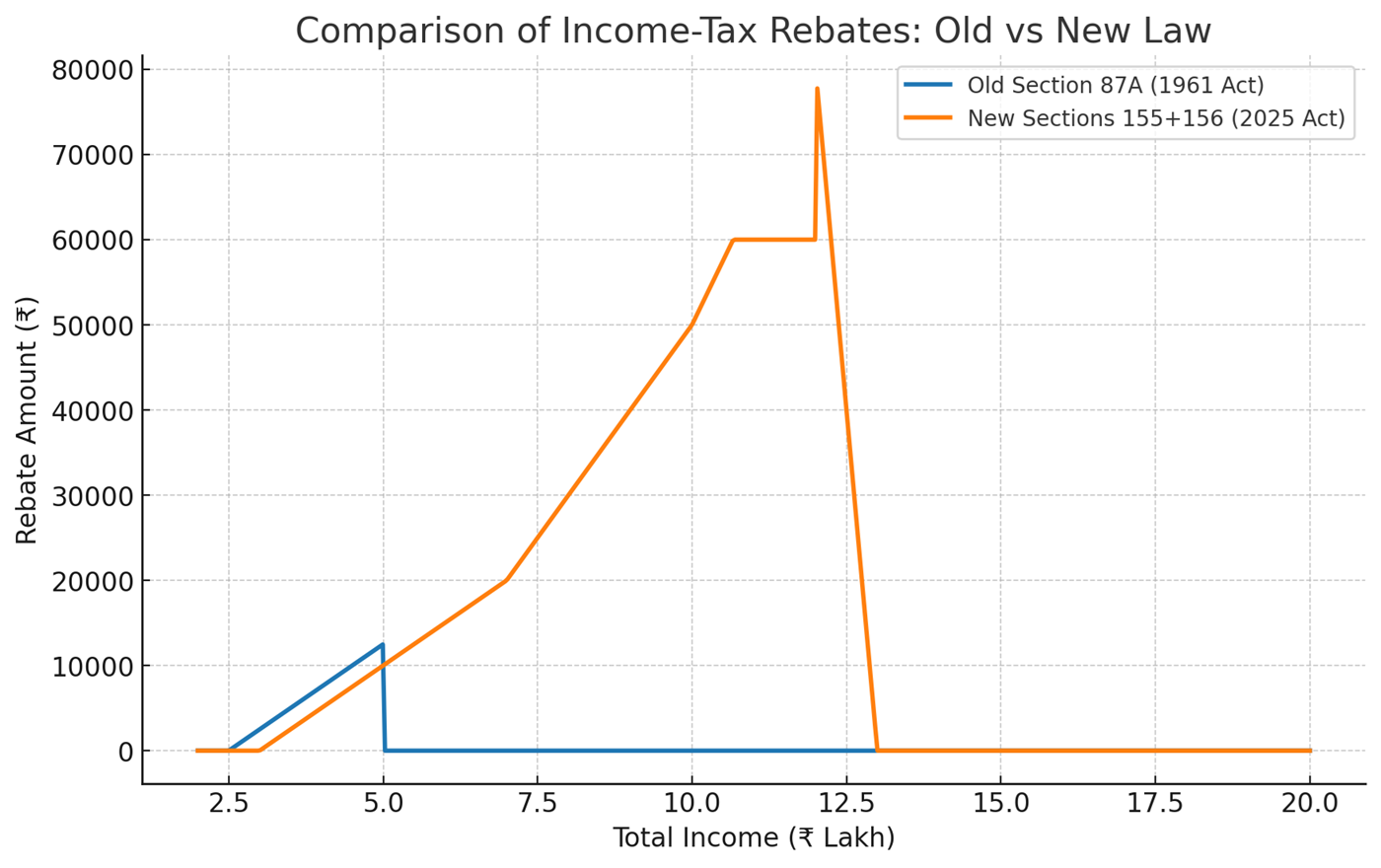

The new Sections 155+156, the rebate extends far beyond ₹5 lakh income, offering substantial relief up to ₹12 lakh, and even a tapering benefit above that, whereas the old Section 87A simply dropped to zero after ₹5 lakh.

Section 156 – Rebate of Income-Tax for Certain Individuals

1. Low-Income Resident Individuals (Total Income ≤ ₹5 lakh)

Eligible for a rebate equal to the lower of:

100% of the income-tax payable (calculated before rebate), or

₹12,500

Applies only when the total income does not exceed ₹5 lakh for the tax year.

2. Residents with Income Up to ₹12 lakh (Chargeable Under Section 202(1))

Entitled to a deduction equal to the lower of:

100% of the income-tax payable, or

₹60,000

3. Residents with Income Above ₹12 lakh (But Chargeable Under Section 202(1))

Rebate is calculated as:

Income-tax payable, minus (total income – ₹12 lakh)

However, this rebate cannot exceed the income-tax payable under Section 202(1).

How Section 155 Integrates with Section 156

Section 155 establishes that when calculating income-tax on total income, you must first compute the full tax amount, then allow deductions under Section 156—but only up to the amount of tax computed (i.e., rebate can’t exceed tax liability).

This protects against rebates exceeding tax liability and ensures no negative or refundable rebates are given.

Practical Examples

Example 1:

Total Income = ₹4 lakh

Compute tax = say ₹20,000

Under Section 156 (income ≤ ₹5 lakh): rebate = min(₹20,000, ₹12,500) = ₹12,500

Final tax payable: ₹20,000 – ₹12,500 = ₹7,500

Example 2:

Total Income = ₹10 lakh (and chargeable under Section 202(1))

Compute tax = assume ₹1,00,000

Rebate = min(₹1,00,000, ₹60,000) = ₹60,000

Final tax payable: ₹1,00,000 – ₹60,000 = ₹40,000

Example 3:

Total Income = ₹15 lakh (chargeable under Section 202(1))

Compute tax = say ₹2,00,000

Income exceeds ₹12 lakh by ₹3 lakh → rebate = ₹2,00,000 – ₹3,00,000 = negative → rebate effectively zero—but limited to not exceed tax, so rebate = ₹0

Final tax payable: ₹2,00,000

Summary Table

| Income Bracket | Rebate Rule Per Section 156 | Effect of Section 155 Cap |

|---|---|---|

| ≤ ₹5 lakh | min(Computed Tax, ₹12,500) | Rebate ≤ Tax |

| > ₹5 lakh & ≤ ₹12 lakh | min(Computed Tax, ₹60,000) | Same cap applies |

| > ₹12 lakh | Computed Tax – (Income – ₹12 lakh), not <0 | Rebate cannot exceed computed tax |

In essence, Section 156 provides graduated rebate thresholds for low- and middle-income resident individuals. Section 155 then ensures these rebates are strictly limited to the actual tax computed, maintaining fiscal balance and preventing excessive benefit.

Old Vs New

1. Old Section 87A (under the 1961 Act)

Who got it: Only resident individuals with total income ≤ ₹5 lakh.

Benefit: Rebate up to ₹12,500, but capped at the tax payable.

Purpose: Wipe out tax liability for low-income individuals.

2. New Structure – Section 155 + 156 (2025 Act)

What changed:

Section 155 = general rule:

Compute tax → apply eligible rebate under Section 156 → rebate ≤ computed tax.

Section 156 = detailed slabs for rebates:

Up to ₹5 lakh → same as old 87A (min of tax payable or ₹12,500).

Above ₹5 lakh and up to ₹12 lakh → new middle-income rebate (min of tax payable or ₹60,000).

Above ₹12 lakh → formula rebate:

Rebate=Tax payable−(Total income−₹12,00,000)

but never negative, and capped at tax payable.

3. Key Differences

| Feature | Old Law (87A) | New Law (155 + 156) |

|---|---|---|

| Low-income relief | Yes, up to ₹12,500 | Yes, same ₹12,500 cap |

| Middle-income relief | No | Yes, up to ₹60,000 |

| Higher income (>₹12L) | No rebate | Partial rebate via formula |

| Universal capping rule | Built into section 87A | Explicitly stated in Section 155 |

| Scope | Single section | Split into “principle” (155) + “details” (156) |

4. Practical Impact

Low-income earners → basically unchanged, still zero tax up to ₹5 lakh.

Middle-income earners (₹5L–₹12L) → biggest winners, as this is a new benefit.

Slightly higher income earners (just above ₹12L) → small cushion to reduce tax jump. In short:

Section 87A was a single-band safety net for low-income residents.

Sections 155 + 156 (2025) turn that into a tiered rebate structure covering low, middle, and near-middle income groups, while Section 155 ensures rebates can’t overshoot the actual tax due.