The ITR-2 is filed by the individuals or HUFs not having income from profit or gains of business or profession and to whom ITR-1 is not applicable. It includes income from capital gains, foreign income, or any agricultural income more than Rs 5,000.

The ITR-2 is a form used by Indian citizens as well as non-resident Indians to file their tax returns with the Income Tax Department of India.

What is ITR-2?

ITR-2 is utilized by individuals and Hindu Undivided Families (HUFs) for filing their Income Tax returns when they do not earn income from business or profession. Typically, it is used by those receiving income from sources like salary, pension, capital gains, and other sources.

Who is eligible to file ITR-2 for AY 2024-25?

ITR-2 forms are used by individuals or Hindu Undivided Families whose total income for the assessment year includes:

- Income from Salary/Pension; or

- Income from House Property; or

- Income from from short-term or long-term capital gains/ sale of investments/ property.

- Income from Other Sources (including Winnings from Lottery and Income from Race Horses)

- Foreign Assets

- Individuals generating income of Rs.5000 and above from agricultural sources

- Individual who is a director of the company or an individual invested in unlisted equity shares

- The total income generated from above-mentioned sources may be Rs.50 lakh and above

If the Income Tax Returns are clubbed with a spouse, minor child etc, then their returns can only be filed together if the sources of income are similar to the ones mentioned above. Should there be a variation in earnings in even one category, the Assessee is liable to fill up a separate and relevant Income Tax Returns Form.

What are the Components of the ITR-2 Form?

The ITR-2 Form is divided into the following categories:

- Part A: General Information

- Part B-TI: Computation of Total Income

- Part B-TTI: Computation of tax liability on total income

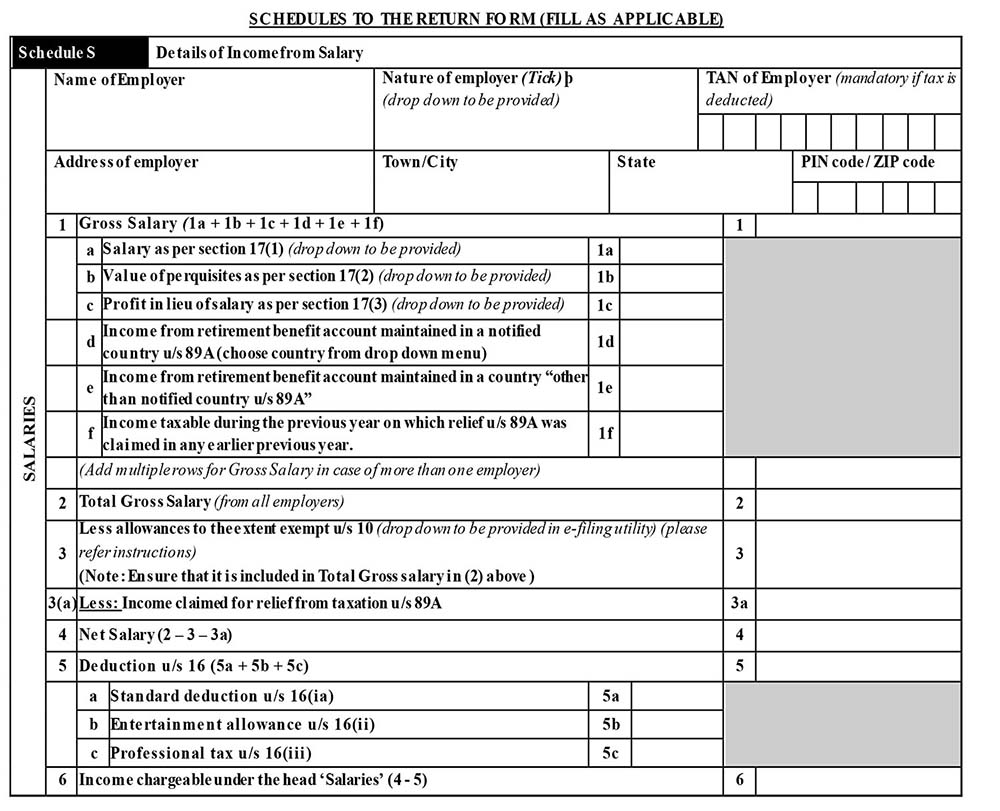

- Schedule S: Details of income from salary

- Schedule HP: Details of income from house property

- Schedule CG: Computation of income from capital gains.

- Schedule 112A: Income from sale of equity share of a company

- Schedule 115AD: Income from sale of equity share of a company (for non-residents)

- Schedule OS: Computation of income from other sources.

- Schedule CYLA: Details of Income after Set off of current year losses

- Schedule BFLA: Details of Income after Set off of Brought Forward Losses of earlier years

- Schedule CFL: Details of Losses to be carried forward to future years .

- Schedule VIA: Deductions under Chapter VI-A (Section)

- Schedule 80G: Details of donations entitled for deduction under section 80G

- Schedule 80GGA: Donations for rural development and scientific research

- Schedule AMT: Computation of Alternate Minimum Tax payable under Section 115JC

- Schedule AMTC: Tax computation under Section 115JD

- Schedule SPI: Income of specified persons (spouse, minor child etc) includible in income of the assessee (income of the minor child, in excess of Rs. 1,500 per child, to be included)

- Schedule SI: Income chargeable to tax at special rates

- Schedule EI: Details of Exempt Income (Income not to be included in Total Income)

- Schedule PTI: Income from business trust or investment fund

- Schedule IT: Statement of payment of advance-tax and tax on self-assessment.

- Schedule TDS1: Details of tax deducted at source on salary.

- Schedule TDS2: Statement of tax deducted at source on income other than salary.

- Schedule FSI: Details of Income from outside India and tax relief

- Schedule TR: Summary of tax relief claimed for taxes paid outside India

- Schedule FA: Details of Foreign Assets and Income from any source outside India

- Schedule 5A: Information regarding apportionment of income between spouses governed by Portuguese Civil Code

- Schedule AL: Liability and assets at year end

- Schedule tax deferred on ESOP: Information of tax deferred on ESOPS

- Part B: TI: Total Income computation

- Part B: TTI: Tax liability computation

- Payment of taxes: Advance tax payment details

- Declaration: Taxpayer’s declaration

- Tax return preparer’s details

Documents Required to file ITR 2

- A copy of last year’s tax return

- Bank Statement

- TDS certificates

- Savings certificates/Deductions

- Interest statement showing interest paid to you throughout the year.

- Balance Sheet, P&L Account Statement and other Audit Reports wherever applicable.

- In case you earn from salary, you require Form 16 issued by your employer

- In case you have earned interest from savings account or fixed deposit, and TDS was deducted, you require a TDS certificate

- You will require Form 26AS for verification of TDS on your salary as well as other source of income

- In case you are living in rented premises, you will require rent receipts for calculating HRA

- In case you have capital gains in shares, you will need summary of profit or loss statement

- To calculate interest income, you will require bank passbook, Fixed Deposit Receipts (FDR)

- In case you have incurred loss and wish to claim it, then you will need relevant documents to support it.

- In case you wish to save tax under Section 80C/ 80G/ 80D or 80GG, then you will need relevant documents to support it

- In case you wish to claim any loss, you will require a copy of ITR-V

Major changes in ITR-2 in AY 2023-24 and AY 2024-25

- Schedule VDA: Income from transfer of Virtual Digital Assets

A new schedule is added to compute income from cryptocurrencies or other virtual Digital assets - Relief u/s 89A: An additional clause has been added related to relief to residents who have income from foreign retirement benefits accounts:

Point No. 1(e)4: Income taxable during the previous year on which relief u/s 89A was claimed in any earlier previous year - Sec 10(12C): In other Exempt Income one new exemption added under Sec 10(12C) – Any payment from the Agniveer Corpus Fund to a person enrolled under the Agnipath Scheme or to his nominee.

- Schedule SI: New point added 115BBH – Income by way of transfer of Virtual Digital assets

- Section 80 CCH: Under Chapter VI A deduction new clause was added- The entire amount contributed by applicants employed by the Central Government to the Agniveer Corpus Fund is eligible for tax deductions.

- ARN: In schedule 80G clause D additional information is required for ARN (donation Reference number)

How to File ITR 2 for FY 2023-24 (AY 2024-25)?

Step 1: Go to the official income tax e-filing website.

Step 2: Enter your user ID (PAN) and password.

Step 3: Enter the captcha displayed on the screen.

Step 4: From the menu, click on ‘e-File.’

Step 5: Click on ‘Income Tax Return.’

Step 6: On the income tax return page, your PAN information will be updated automatically.

Step 7: Choose ‘Assessment Year,’ followed by ‘ITR Form Number.’

Step 8: Choose ‘Filing Type‘ and then ‘Original/Revised Return.’

Step 9: Click the ‘Continue‘ button.

Step 10: Go through the instructions properly. Then, complete the ITR-2 form by entering information in all applicable and necessary fields.

Step 11: To avoid losing data due to session time-out, ensure to choose the ‘Save Draft‘ option regularly.

Step 12: In the ‘Taxes Paid’ and ‘Verification’ sections, select an appropriate verification option

Step 13: To verify your ITR, select an appropriate option.

Step 14: Click on the ‘Preview and Submit’ option.

Step 15: Check if your ITR information is accurate.

Step 16: Click the ‘Submit‘ button.

FAQs

Who cannot file ITR-2 for AY 2024-25?

- Any individual or HUF having income from business or profession

- Individuals who are eligible to fill out the ITR-1 form (Sahaj)

Major updates in ITR-2 in AY 2023-24 and AY 2024-25?

- Section 10(12C) introduces a new exemption for payments received from the Agniveer Corpus Fund, applicable to individuals enrolled under the Agnipath Scheme or their nominees.

- A new section called Schedule VDA has been added to report income from transactions involving cryptocurrencies or other virtual digital assets.

- Schedule SI now includes a new point, 115BBH, specifically for reporting income generated from the transfer of Virtual Digital Assets.

- Schedule 80G now mandates disclosure of the ARN (donation Reference number) for donations, enhancing transparency and verification.

- An additional clause under Relief u/s 89A now addresses residents receiving income from foreign retirement benefits, requiring disclosure of taxable income for which relief was previously claimed.

- Central Government employees can now claim deductions under Section 80 CCH for the entire amount contributed to the Agniveer Corpus Fund.

- Schedule 80G now mandates disclosure of the ARN (donation Reference number) for donations, enhancing transparency and verification.