A double-entry bookkeeping system is where a corresponding entry is made for every transaction, i.e. debits and credits. The basis of the double-entry bookkeeping system is that every transaction has two parts and affects two ledger accounts. The double-entry system of bookkeeping deals with two or more accounts for every business transaction.

For example, if a company enters into a transaction of borrowing money from a bank, there will be two entries as an asset and a liability. This is because it will increase the assets for the cash balance account and also increase the liability for the loan payable account.

Thus, all financial transactions have an opposite and equal entry in at least two different accounts. The double-entry system of bookkeeping is widely used, and it includes detailed descriptions of the services and products, expenses, income, bad debt, loans, etc.

One of the fundamental equations of accounting is – Assets = Liability + Equity. The total of both sides of the equation should be the same. If the total assets are not equal to the total liabilities plus capital, then there is a mistake in the books of accounts. Thus, every transaction has two entries, and if the liabilities increase, then the assets must also increase for the books to be balanced.

What Is Double Entry?

Double entry is a bookkeeping and accounting method, which states that every financial transaction has equal and opposite effects in at least two different accounts. It is used to satisfy the accounting equation:

Assets=Liabilities+EquityAssets=Liabilities+Equity

Principles of Double-Entry System of Bookkeeping

The principles to be followed while recording the double-entry system of bookkeeping are as follows:

- Debit is written to the left, credit on the right

- Every debit must have a corresponding credit

- Debit receives the benefit, and credit gives the benefit

There are rules to be kept in mind while posting the double-entry transactions in the bookkeeping process. The following are the rules for the different types of accounts:

- For Personal Accounts: Debit the receiver, credit the giver

- For Real Account: Debit what comes in, credit what goes out

- For Nominal Account: Debit all the expenses, credit all the incomes

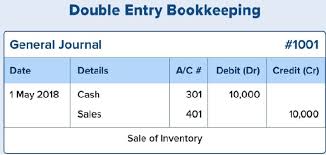

Journal Entries of Double-Entry System of Bookkeeping

Every transaction entered in a journal involves a debit entry in one account and a credit entry in another account. Thus, every transaction should be recorded in two accounts. The transaction recorded in two accounts reflect the debit in the account that receives value and credit in the other account that has given value.

The main rule for the double-entry system entry is ‘debit the receiver and credit the giver’. The debit entry for a transaction will be on the left side of the general journal, while the credit entry will be on the right side of the journal. The total of debits and credits should be equal for the transactions to be balanced.

The following table shows an example of the double-entry of transactions in a journal.

| Sl. No. | Date | Particulars | Debit (Dr) | Credit (Cr) |

| 1 | 1/7/2021 | Salary Cash A/c (Being salaries paid) | 20,000 | 20,000 |

| 2 | 5/7/2021 | Electricity Bill Cash A/c (Being electricity bill paid) | 1,000 | 1,000 |

| 3 | 8/7/2021 | Vehicle BankA/c (Being vehicle purchased) | 50,000 | 50,000 |

In the above table, the first entry is the entry of salary paid. As the salary is a nominal account, the rule is to debit all expenses and cash, being a real account, is credited as the cash payment reduces the asset.

The next entry is the electricity bill that is paid. Since the electricity bill is a nominal account, the expense of the bill is debited, and the cash account is credited, being a real account.

The third entry is of vehicle bought by the business. Since the vehicle is an asset and a real account, the incoming asset (vehicle) is debited, and the cash paid through a bank account for the vehicle is credited.

The above examples of journal entries show the double-entry of transactions, as per the rules of debit and credit for the respective accounts.

FAQs

What Is the Disadvantage of the Double-Entry Accounting System?

The primary disadvantage of the double-entry accounting system is that it is more complex. It requires two entries to be recorded when one transaction takes place. It also requires that mathematically, debits and credits always equal each other. This complexity can be time-consuming as well as more costly; however, in the long run, it is more beneficial to a company than single-entry accounting.

What Is the Difference Between Single-Entry Accounting and Double-Entry Accounting?

In single-entry accounting, when a business completes a transaction, it records that transaction in only one account. For example, if a business sells a good, the expenses of the good are recorded when it is purchased, and the revenue is recorded when the good is sold.

With double-entry accounting, when the good is purchased, it records an increase in inventory and a decrease in assets. When the good is sold, it records a decrease in inventory and an increase in cash (assets). Double-entry accounting provides a holistic view of a company’s transactions and a clearer financial picture.