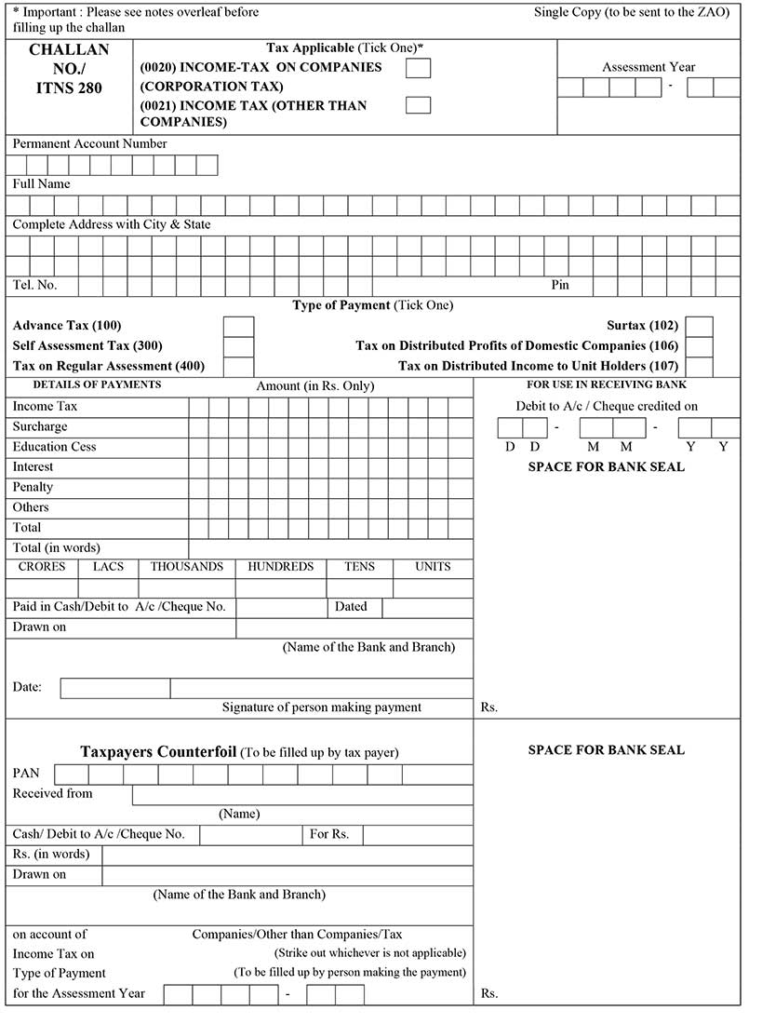

Challan 280

Introduction Income tax payment is a vital component of every taxpayer’s life. Whether you are a salaried employee or a business owner, you need to pay your taxes on time to avoid any penalties or legal complications. One of the most popular methods for making income tax payment is using Challan 280. Challan 280 is […]